Why it’s important to review your renewable energy property and business interruption policies

The renewable energy industry and renewable energy projects, like many businesses, are experiencing the effects of the highest inflation rates in a generation.

Across the board, price surges are affecting the market value of assets. Supply shortages and delays are prolonging rebuild times. They are also increasing the potential total cost of operational stoppages.

This makes it crucial for you to review your insured values and insurance policy wordings. This will help you determine whether your insurance and programs remain adequate and work out how much cover you need.

While the drivers and impacts of inflation can vary, several factors could be affecting your business. These factors may be driving increases in asset valuation. These factors are also contributing to:

- Supply chain disruptions

- Commodity price increases

- Labour costs and availability

- Higher manufacturing costs

- Rising finished goods costs

- Exchange rate instability.

As the rebuild costs and expenses to recover after a loss increase, insurers are requesting updated property values from their policyholders. This information is needed to adjust their catastrophe modelling. Some are also reviewing premiums to determine whether they remain adequate for current risks. Amid heightened underwriter scrutiny it is essential to develop and maintain reliable asset values. This should be done using consistent and sensible methods.

For renewable energy asset owners and investors, material damage and business interruption insurance should serve as a crucial safety net. This coverage is vital for protecting against potential losses. These help protect your property assets and business for loss of income against unforeseen events. In the current climate of increasing asset reinstatement values and wholesale energy prices soaring, underinsurance is one of the major risks that is facing the renewable energy industry.

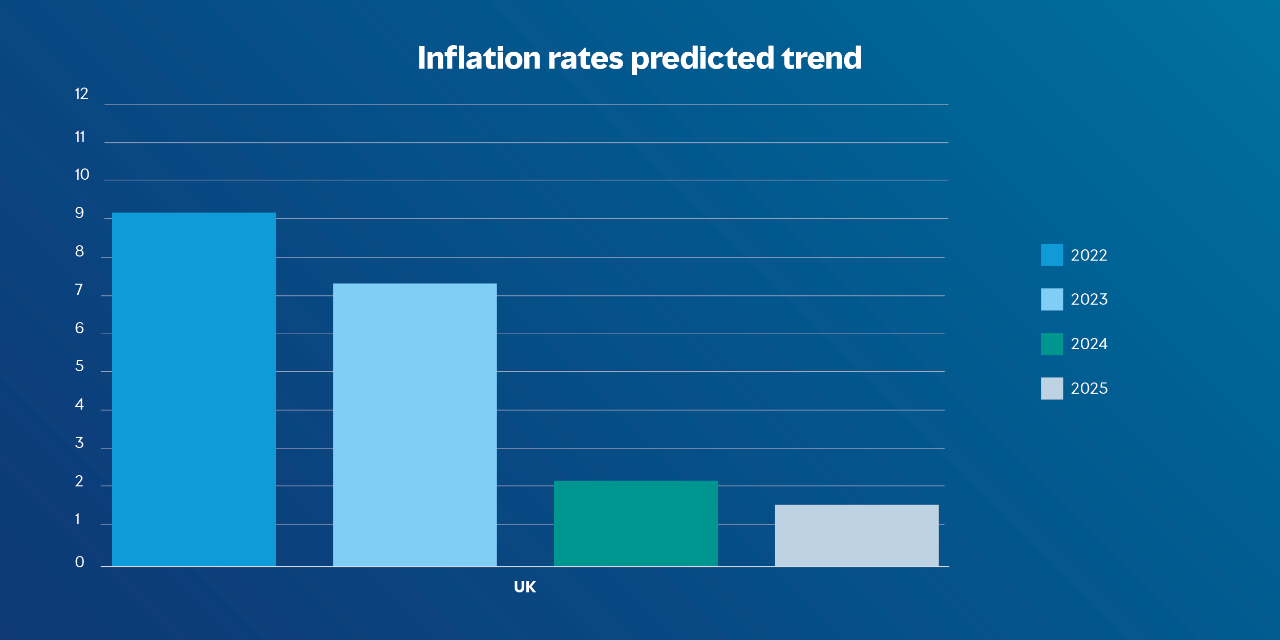

Inflation rates and costs drive underinsurance concerns

The surge in inflation is slowing. However, inflation is still expected to impact property and business interruption values across all industries and geographies.1

Construction prices and building costs have also increased significantly over the past several years.

In this environment, it’s more important than ever to be mindful of the risks of underinsurance that may impede your business’ recovery. Claims payments could be capped below the actual present value of lost assets. Additionally, stipulations in policy terms could lead to further implications if you’re underinsured.

Potential consequences of underinsurance

Underinsurance typically occurs when the declared values of assets and exposures fall below the actual values. Assets such as:

- property;

- building;

- contents;

- wind farm turbines;

- solar plants;

- battery energy storage solutions;

- and Anaerobic digestion plants.

This can have significant potential consequences, including:

1. Policy loss limits

If the value of insured assets goes up, but the relevant loss limits aren’t appropriately increased, you may not have full indemnity. This could be problematic if your business suffers a major loss that exceeds the policy loss limit.

2. Property – application of average or underinsurance clauses

Legislation (such as the Insurance Act 2015), insurance market practice, and policy wording vary globally. But average or underinsurance clauses will apply in most countries. Policy wording usually includes at least one average provision. These clauses typically allow insurers to proportionally reduce the value of a claim.

In the event of your business being underinsured, your insurer may proportionately reduce the amount it is obliged to pay you. They’ll base this on the difference between the insured value and the actual value of the lost or damaged asset.

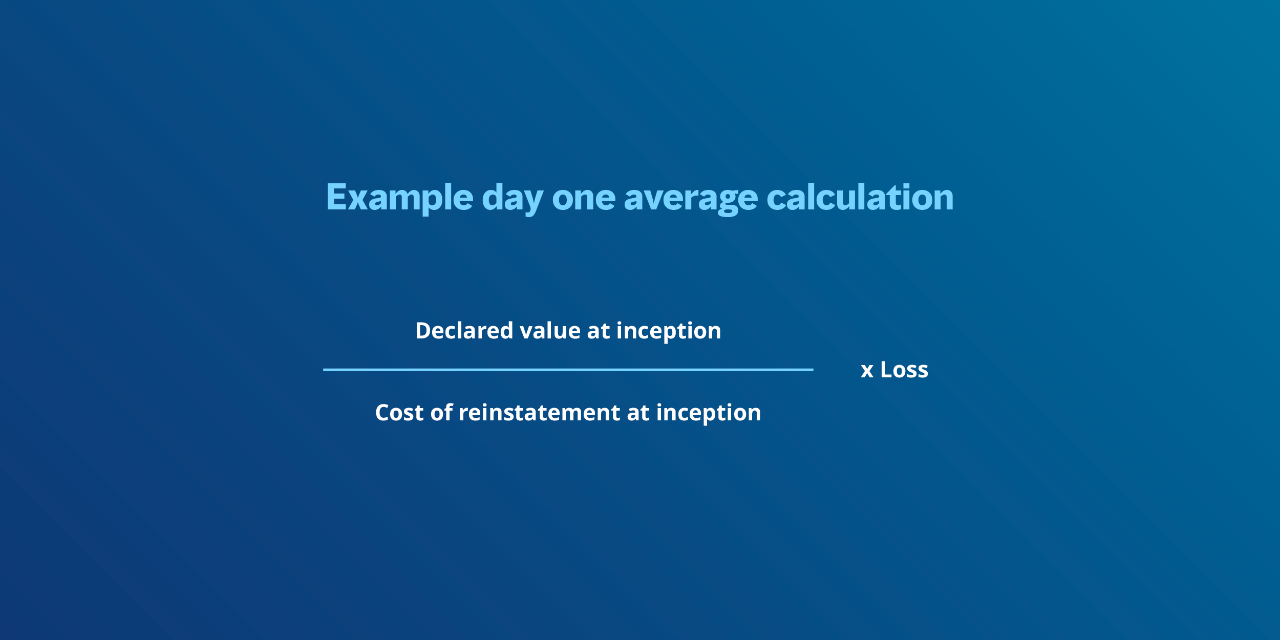

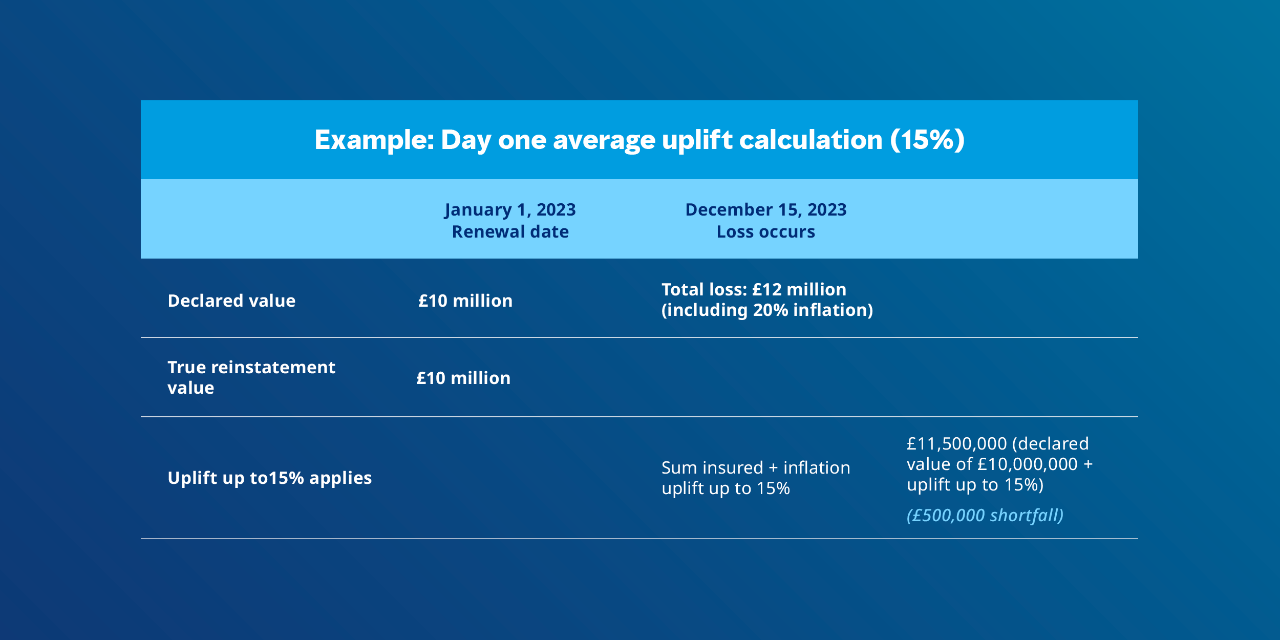

3. Explanation of common average provisions and its implications

The insured business declares values on a reinstatement basis on the first day of the policy period. But the insurer pays the cost of repair or reconstruction at the time of the loss. The accuracy of the values is assessed retrospectively to determine whether the value declared by the business was accurate at the start of the insurance period.

If the values declared on day one of the policy period are found to be inadequate, then the insurer may be able to reduce the claims payment. To avoid underinsurance deductions, make sure you provide accurate values to your insurer at the start or renewal of the policy.

A day-one uplift can, in some policies, be included to protect against inflation, for example an uplift of up to 15%. However, market practices differ across countries and can also vary depending on the specific policy wording. In the example below, the declared values are increased with more than the uplift protection provided in the policy. If uplift protection isn’t provided or is insufficient, insured values and policy limits must be adjusted mid-term. This adjustment is necessary to secure adequate insurance protection.

Example calculation:

4. Business interruption – adequacy of indemnity period

Some business interruption policies include a maximum indemnity period. This is the maximum duration for which insurers will pay business interruption losses following an insured event. These are usually set at 12, 18, 24, 30, or 36 months following the loss event.

Delays resulting from damaged property not being reinstated before the business interruption indemnity period expires may lead to uninsured extra costs and loss of revenue or profit. A 12-month indemnity period may not be adequate in today’s environment. As it may run out before your business can get supplies and complete rebuilding.

Additionally, many businesses are only just returning to pre-COVID-19 levels of activity. At the same time they need to increase their prices to contend with higher payroll costs.

This volatility can result in a significant shortfall in the amount your business would’ve expected to receive in the event of a claim. Supply and labour shortages could lead to shipment delays and lengthy construction timeframes. Therefore, you should consider reviewing traditional indemnity periods. And, where necessary, request an extension.

5. Business interruption – declaration-linked

Some business interruption policies include a declaration-linked mechanism that allows for some growth. For example, a 33.33% increase in the estimated gross profit over the indemnity period. This provides some protection against inflation. Yet it may still be inadequate for rapidly growing and changing businesses during a significant inflationary period.

Take action now

Recent research has found that 80% of UK commercial properties are underinsured. With an estimated underinsurance total value of £340 billion. Existing cover for buildings insurance falls short. On average underinsured buildings are covered for just 68% of the amount they should be.2 Whilst this research is based on general property, we can assume that renewable assets will also follow a similar trend.

This underinsurance gap isn’t something you can afford to ignore. It can have a significant financial impact if the time comes to make a claim.

Make sure you seek advice from experienced professionals who have a proven track record in the renewable energy sector.

Real-world insight that we don't share anywhere else

Get access to exclusive help, advice and support, delivered straight to your inbox.

Got a burning question?

Let us know what you'd like to learn more about, your question may help others too! An adviser will be in touch to answer your question shortly.